Photo by the author

Microfinance, fixed costs, and the indispensability of the state

Staying focused these days is a discipline in itself. The American-Iranian deal has lately dominated the headlines. Inflation is back as a concern in the United States and Europe. Equities, bonds, and gold are moving in different directions, each telling a different story about where markets think the world is heading. And then there is Lebanon: the Israeli war, the state’s timid attempt to be in charge, and the endless political drama are always in the background for those of us emotionally connected to it. Were it not for the inconvenient schedule of many of the matches, the World Cup would have completed the list of distractions.

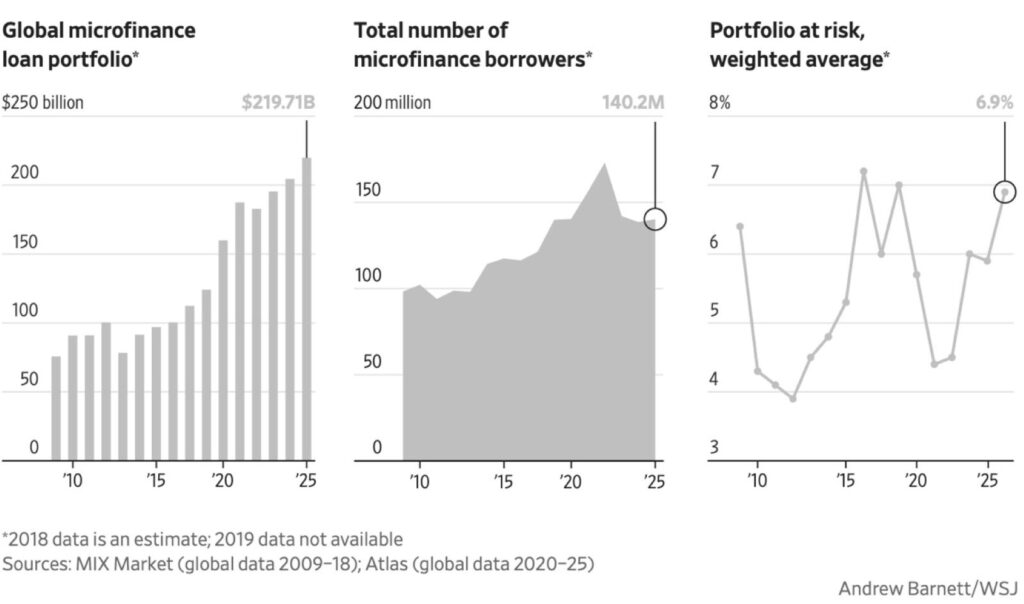

It was in the middle of all this distraction that a recently published Wall Street Journal article caught my attention. “Hundreds of Billions in Loans Didn’t Make a Dent in Global Poverty” is a long-reported account of the reckoning with microfinance. Its findings are blunt: lenders around the globe had $219.7 billion in outstanding microloans to more than 140 million borrowers last year, yet two decades after Muhammad Yunus accepted the Nobel Peace Prize, randomized controlled trials have found no significant improvement in the economic conditions of most borrowers. Repayment crises have erupted from Bosnia to India to Cambodia. Interest rates top 100% in parts of Latin America. Lenders founded by Oxfam, Catholic Relief Services, and EU aid projects have been sold to commercial banks and private equity. Yunus himself warned, years ago, that for-profit microfinance lenders had begun to resemble the loan sharks they were meant to replace.

Reading it brought me back to my undergraduate and postgraduate years in economics, when I first encountered Yunus’s Banker to the Poor. It was an inspiring book, and it was meant to be. The story of the $27 that cleared the debts of bamboo-stool makers in a Bangladeshi village during the 1974 famine was the founding myth of an entire industry and of an entire way of thinking about development.

The world that believed in microfinance

It is worth remembering what kind of world produced such ideas. The idea that access to finance could narrow the poverty and inequality gap belonged to an era that still had confidence in the comparative advantage of international development assistance and in the multilateralism constructed after the Second World War. Development was a project. Institutions were its pillars, and capital, properly channeled, was its main instrument. Microfinance fit perfectly into that worldview: it was capitalism’s cure for poverty. It was market-friendly, scalable, and morally satisfying.

That world has largely been dismantled, largely by the populist assault on the institutions and ideas that sustained it. Development assistance is in retreat. Multilateralism is on the defensive everywhere. However, Microfinance kept growing, now fueled not by developmental idealism but by Wall Street’s appetite for high yields and low defaults, as the WSJ article shows.

Does microfinance really make a difference?

Throughout my professional career, I was involved in a few microfinance initiatives, and over time I developed what I admit is an unpopular, even skeptical, view.

In countries where the state fails to provide basic services such as electricity, water, security, and infrastructure, citizens and firms must procure these services privately. The defining burden on micro and small enterprises in such environments is not access to capital. It is the heavy burden of fixed costs. The generator, the water truck, or informal payments are regressive by nature and fall heavily on small producers or traders.

Microfinance can never fix this problem; at best, it only postpones it. If the only way out of the fixed-cost trap is to expand production in order to spread those costs over greater output through economies of scale, then microfinance is, by design, the wrong instrument. The capital needed to reach scale is precisely the capital that microfinance does not and cannot provide. A $500 loan does not buy economies of scale. It buys a few months of survival and an obligation to pay with interest.

My skepticism was never about Yunus’s original idea. The Grameen model emerged in a context of near-zero fixed costs: women making bamboo stools at home, whose only constraint was the predatory cost of raw materials borrowed from a middleman. The problems emerged when this model was mainstreamed: assuming that what worked for a stool-maker in a Bangladeshi village would work for an African farmer collateralizing his family’s land, or a shop owner in Tripoli paying three electricity bills: one to the state utility that delivers nothing, one to the generator cartel, and now one for solar panels.

The unescapable role of the state

Which brings me to the uncomfortable conclusion the development industry has spent decades avoiding: poverty alleviation and narrowing the inequality gap require strong, capable governments and continuous fiscal and budgetary commitment. There is no financial product that substitutes for this. International organizations and charities tried, in effect, to subsidize state incompetence and bad governance through various financing schemes that routed capital around the state rather than building it. The World Bank and other international organizations reacted to a brain drain from the Lebanese public sector and the military during the post-2019 economic crisis by providing cash stipends, thereby reducing the political elite’s incentive to find solutions to the crisis. The burden of the crisis simply shifted from the ruling elite to the international community.

The lesson of forty years is that you cannot escape the state trap. The need for the state always reasserts itself, as best captured by the question Lebanese have been asking for decades: Wayn el-dawleh? Where is the state?

Take a look at Lebanon’s rooftops, and you have your answer. A few years ago, the World Bank, in a publication, celebrated Lebanon as one of the world’s leading producers of off-grid solar energy, calling it a remarkable achievement. It was nothing of the sort. The rooftop panels covering Beirut’s apartment blocks or the roofs of traditional village houses are not evidence of an environmental awakening; they are a coping mechanism, the privatized response of households to the state’s failure to provide electricity. Each panel is a small monument to institutional collapse, financed most of the time by remittances.

The logic extends to social policy itself. You can never credibly claim to fight poverty when your social protection programs or cash transfers are funded by loans rather than by the state’s budget. A safety net financed by external debt is not social protection. The poor might benefit today, but the future generations who will have to repay the debt will definitely blame today’s poor for what they inherited.

The Same Vicious Circle

Returning to the article’s reporting, one can detect a familiar pattern to anyone who studied the political economy of the Global South. The Cambodian mother taking a second loan to service the first, or the farmer borrowing from neighbors and loan sharks to keep up with the microfinance lender, is a common observation, regardless of geographic, ethnic, or national origin. States are borrowing to finance cash transfers to the poor or to increase public-sector salaries because they cannot afford to do so from their own budgets. It is the same pattern: debt substituting for income in the household and debt substituting for fiscal capacity at the state level. The same trap on a different scale.

Microfinance was never merely a financial product. It was the household-level component of a development paradigm that held that the state could be bypassed, that markets and NGOs could channel capital to good causes, and that, as a result, they could deliver what politics had failed to deliver. The solar panels, the generators, the microloans: none of this is development. It is privatized coping mechanisms, dressed up in the language of empowerment and resilience.

The hard lesson, then, is the oldest in development economics: Poverty is not the result of people being unbanked or lacking access to finance. It is the outcome of weak institutions, low state capacity, inadequate public goods, and a social contract that fails to generate sustainable growth. Overcoming poverty requires more than expanding access to loans. It requires building an equitable fiscal system, enforcing rights and the rule of law, and modernizing labor markets. Around $220 billion has been spent on microfinance, and the verdict is hard to avoid: finance can support development, but it cannot compensate for governance failure, not in Dhaka or Battambang, and definitely not in Beirut.

Khalil Gebara is an academic and researcher.

The views in this story reflect those of the author alone and do not necessarily reflect the beliefs of NOW.